Mortgage Readiness: Secure a Mortgage

Andy Thomson on 06 March 2025

For many first-time buyers, securing a mortgage can feel overwhelming. Lenders scrutinise your finances, assessing factors you may not have considered. This is where Klink’s Mortgage Readiness Feature comes in - helping first-time buyers and renters understand their financial position and improve their chances of mortgage approval.

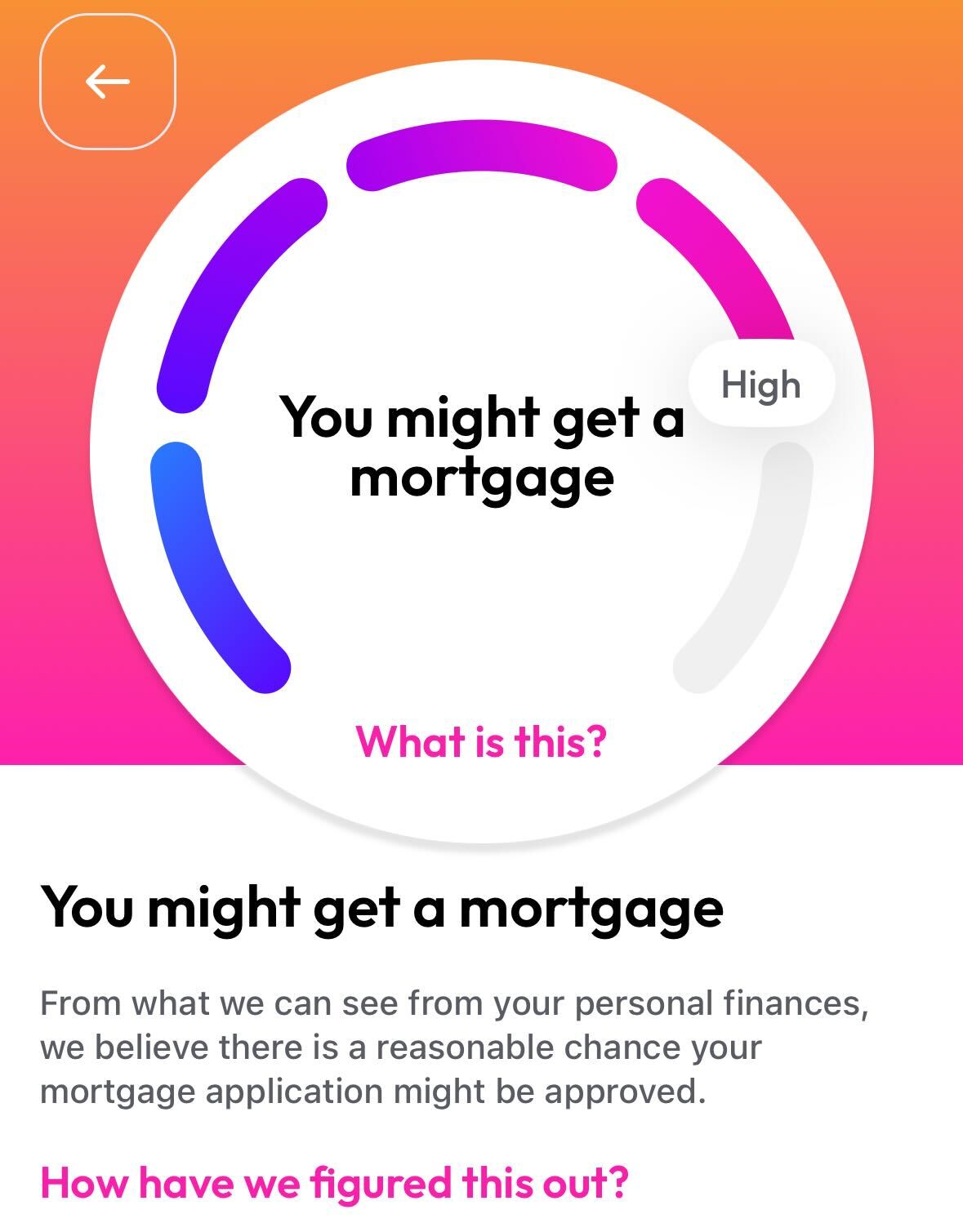

Much like a credit report, but tailored to your banking activity, Klink’s Mortgage Readiness Feature analyses your finances using open banking data to give you a clear, actionable mortgage readiness score. This allows you to see where your strengths are and which areas might need improvement before applying for a mortgage.

What is the Klink Mortgage Readiness Feature?

Klink’s Mortgage Readiness Feature provides an overall score, based on a detailed analysis of 11 key financial factors, offering a breakdown of what is boosting or harming your score.

Unlike traditional mortgage checks, which may only assess income and credit scores, Klink goes further by evaluating spending patterns, affordability, and financial habits. By connecting all your bank accounts, Klink can provide a comprehensive financial health check, helping you take proactive steps towards mortgage approval.

How Does It Work?

Once you link your bank accounts, Klink analyses transactions and spending behaviour, assigning a weighted score across 11 financial factors. These are designed to reflect lender concerns and help you spot potential red flags before a formal mortgage application.

Key Factors in Your Mortgage Readiness Score

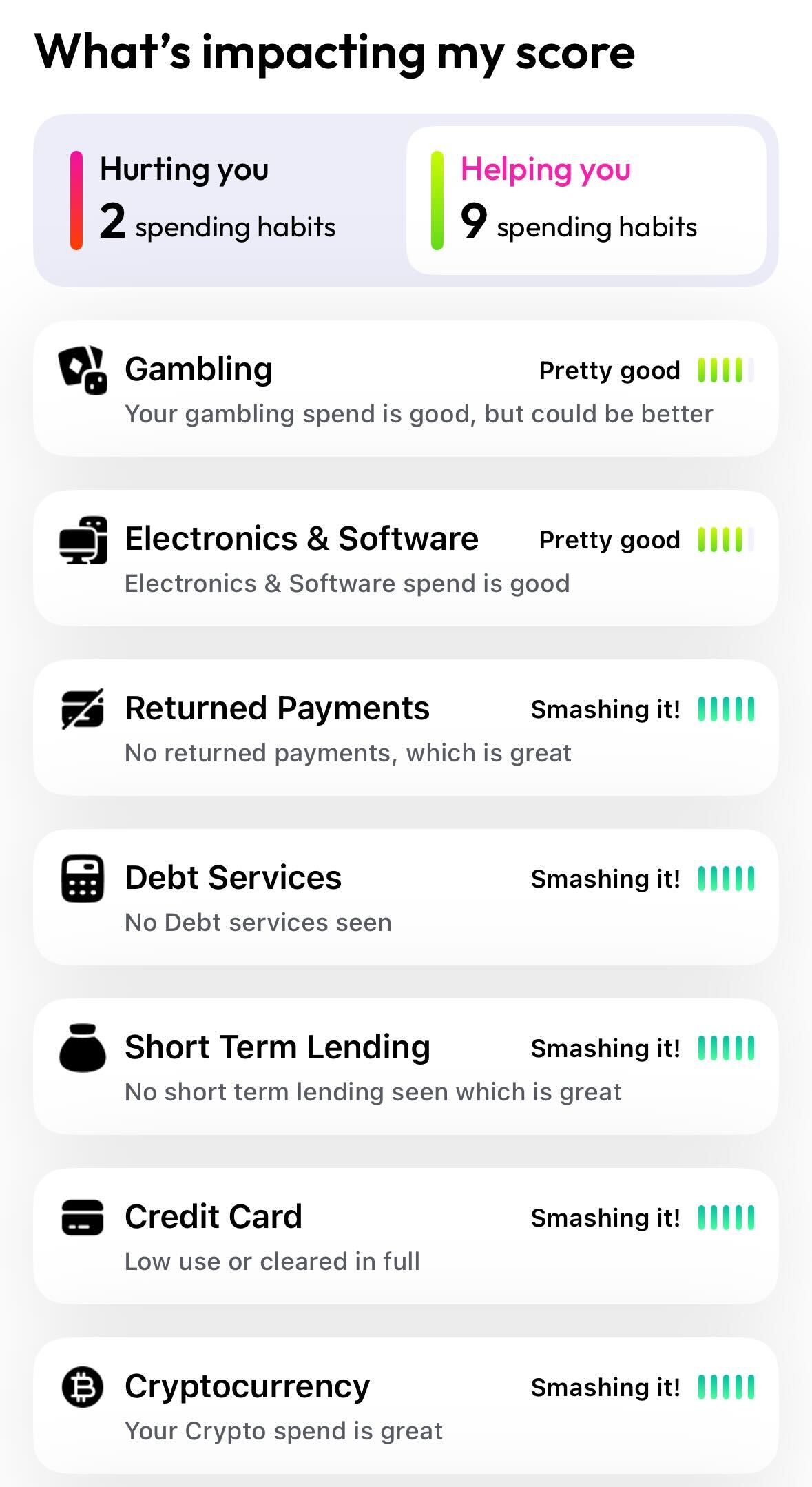

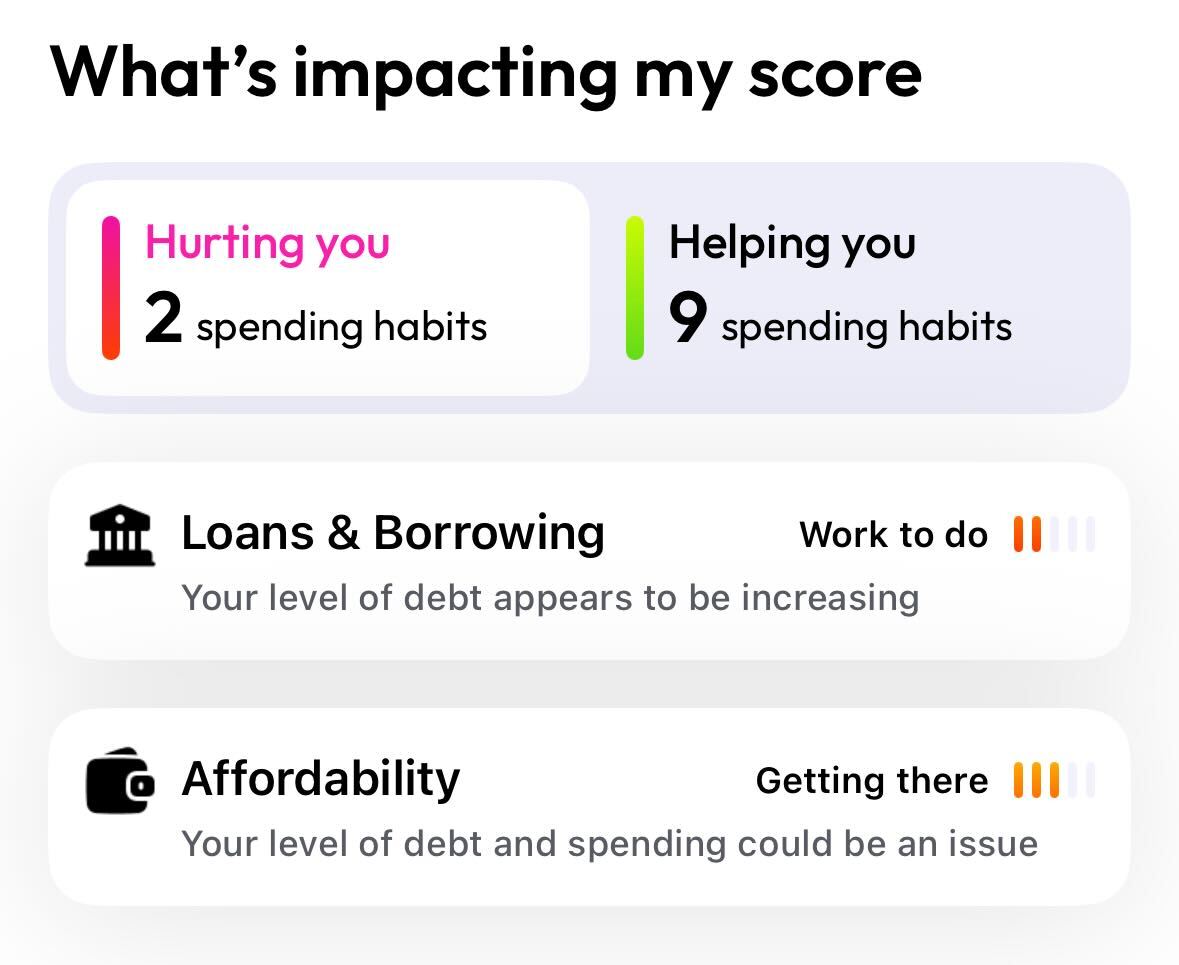

Each of these categories is scored from very low to very high and contributes to your overall rating:

- Gambling – Monitors gambling activity and flags if this might be a concern for lenders. Excessive gambling can be seen as a financial risk.

- Electronics & Software – Assesses spending on digital goods, particularly in-game purchases, to detect addictive spending patterns similar to gambling.

- Returned Payments – Checks for declined or returned payments, with recent incidents being more concerning than older ones.

- Debt Services – Identifies payments to debt collectors or debt management plans, which could limit mortgage options.

- Short-Term Lending – Flags reliance on payday loans or high-interest lending, which signals financial instability.

- Credit Card Usage – Evaluates credit card spending, looking at excessive balances and reliance on revolving debt.

- Cryptocurrency – Highlights high crypto transactions, as many lenders do not accept cryptocurrency as a valid deposit or consider it a secure savings method. Some lenders will also treat high crypto spend similar to that of gambling so be careful!

- Cash Transactions – Examines excessive cash withdrawals or large unexplained deposits, which may require further lender scrutiny.

- Buy Now Pay Later (BNPL) – Tracks frequent use of BNPL services, which can impact perceived affordability. As well as flags for poor money management.

- Loans & Borrowing – Assesses borrowing trends to determine if debt levels are increasing or decreasing over time.

- Affordability – Uses open banking data to compare declared income against actual expenditure, ensuring financial habits align with mortgage goals.

Why is This Important for Mortgage Approval?

Traditional mortgage lenders typically review credit scores, salary, and bank statements when assessing an application. However, they also examine spending behaviour, debt levels, and financial stability. Many mortgage applications fail because applicants are unaware of certain financial habits that raise red flags.

For example:

-

High BNPL spending or gambling transactions can make lenders nervous.

-

Frequent returned payments may suggest financial struggles.

-

Short-term loans or debt repayment plans can signal financial distress.

Klink helps you identify these risks before applying, giving you time to adjust your financial behaviour and improve your readiness score. By knowing where you stand, you can make informed decisions about how to increase your chances of getting approved.

Proactive Mortgage Planning with Klink

Unlike traditional assessments that only highlight issues after applying for a mortgage, Klink allows you to see and fix potential problems beforehand. This proactive approach gives you control over your financial profile, helping you avoid last-minute rejections and secure better mortgage rates. Instead of being caught off guard by a lender’s decision, you can work towards making your finances mortgage-ready well in advance.

By using Klink to track and improve your score, you can address potential barriers months before submitting an application. Whether it’s reducing short-term debt, limiting BNPL usage, or adjusting spending habits, Klink provides clear, actionable insights that put you in the best position to succeed.

Taking control of your mortgage readiness doesn’t just mean a higher chance of approval - it could also mean access to better mortgage deals, lower interest rates, and improved affordability.

Getting Mortgage Ready with Klink

If you’re serious about buying a home, using Klink’s Mortgage Readiness Feature could give you a significant advantage. By regularly tracking your score and improving weak areas, you can boost your mortgage chances before even approaching a lender.

Download Klink today and take control of your mortgage journey. A better score means a better chance of securing the home you want.

Klink does not provide financial advice, the mortgage readiness tool is to help provide better insights as to what a mortgage lender may think is a concern and how to improve it. For it to be most accurate it needs all your bank accounts connected and Klink recommends always speaking to a mortgage broker. The mortgage readiness tool is not a guarantee that you will be able to or not able to obtain a mortgage.

Share:

Categories

Recent posts

Tag Cloud

Related Blogs

MORTGAGE READINESS

Jul 17 · 4 min read

The journey from viewing dream properties to getting the keys can be interrupted by an unexpected hurdle: a rejected mortgage application. Here are ten common reasons why your mortgage application can be rejected.

Read More

MORTGAGE READINESS

Jan 24 · 4 min read

If you’re a first-time buyer or a renter pondering the possibility of trading rent payments for mortgage repayments, the good news is that the answer isn’t as daunting as you might think

Read More

MORTGAGE READINESS

Jul 17 · 4 min read

Let's dive into the dark arts of credit scores and uncover the secrets to finding yours.

Read MoreMORTGAGE READINESS

Jul 17 · 4 min read

10 Surprising Reasons Your UK Mortgage Application Got Rejected (And How to Fix Them!)

The journey from viewing dream properties to getting the keys can be interrupted by an unexpected hurdle: a rejected mortgage application. Here are ten common reasons why your mortgage application can be rejected.

Read More

MORTGAGE READINESS

Jan 24 · 4 min read

Can I Get a Mortgage?

If you’re a first-time buyer or a renter pondering the possibility of trading rent payments for mortgage repayments, the good news is that the answer isn’t as daunting as you might think

Read More

MORTGAGE READINESS

Jul 17 · 4 min read

Your Mission: Finding Your Credit Score in the UK

Let's dive into the dark arts of credit scores and uncover the secrets to finding yours.

Read More

Want to know more about Klink?

Make a date with home ownership by joining our growing community